Pharos: Free and Open Research-Grade Stablecoin Intelligence

Pharos tracks stablecoin pegs, safety scores, liquidity, early warnings, and systemic risk as a free open-source public good.

Pharos tracks stablecoin pegs, safety scores, liquidity, early warnings, and systemic risk as a free open-source public good.

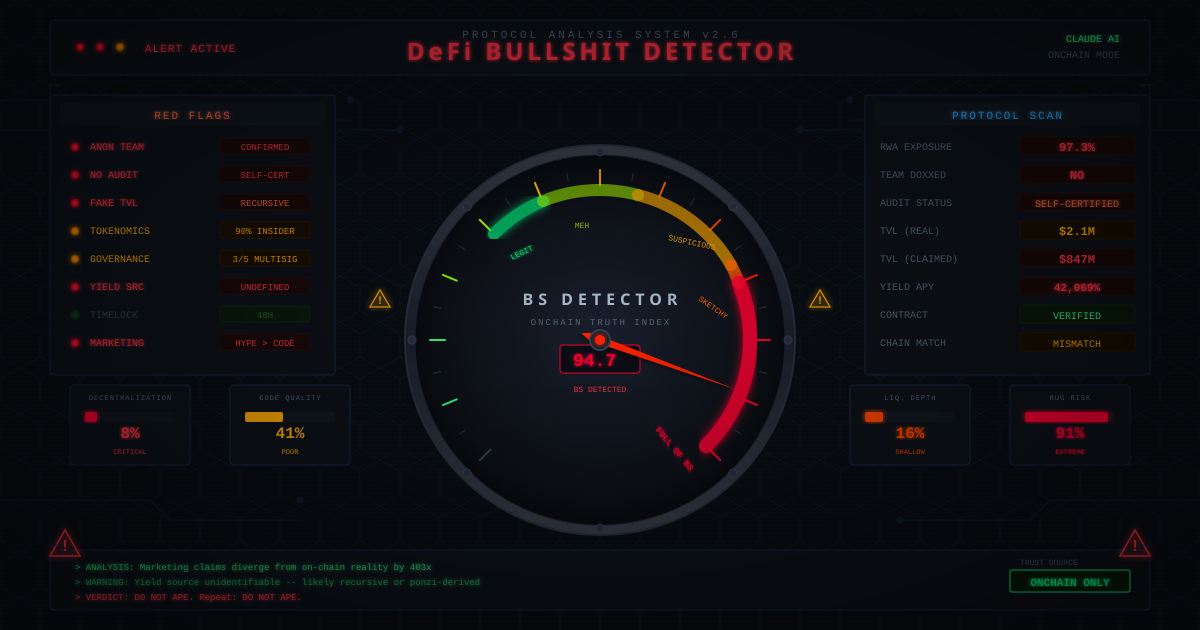

Setup guide for a Claude-based DeFi research assistant that checks onchain reality, team history, and risks before trusting protocol marketing.

Why Polaris is being built as a counterparty-free, immutable stablecoin system after years of watching DeFi stablecoins drift toward TradFi dependencies.

The development of the veNFT infrastructure layer with Autopilot, 40Acres, and haiVELO: automation, collateral, and yield enhancement.

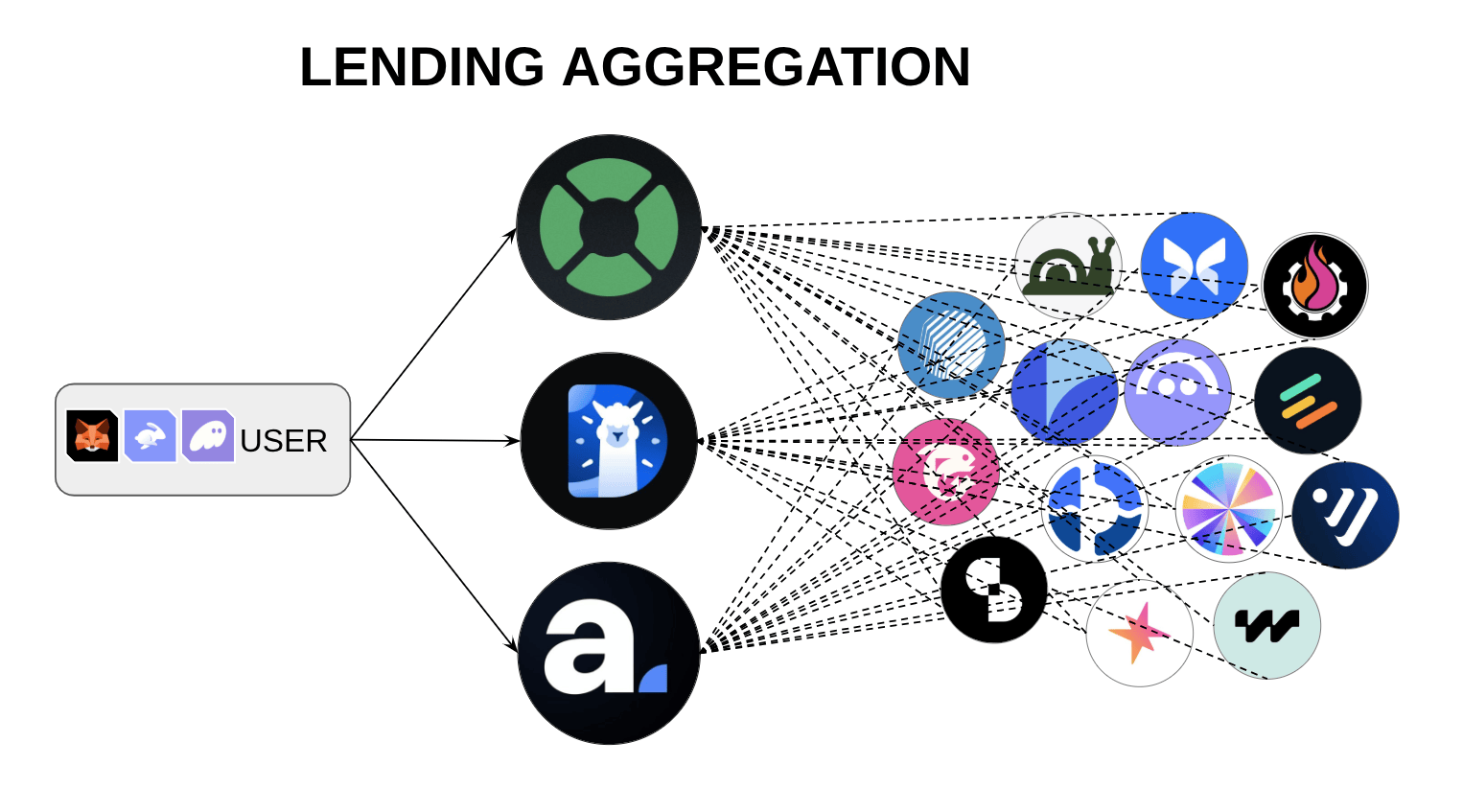

The real edge isn’t in finding the rate; it’s in owning the rails that connect them all.

A look at debt-driven liquidity for pegged asset swaps, and why constant incentives may not be the best way to sustain deep stable liquidity.

Exploring a novel protocol offering no funding fee no liquidation leverage with convex returns, and announcing my involvment.

Shining a light on DeFi’s dirty secret: the curation layer crisis - and what can we do to address it.

New models are being explored both for CDP protocols and money markets, and some protocols are even merging the two into one: is this a lending protocol renaissance?

Why the Velodrome model improves veCRV-style alignment between LPs, tokenholders, and projects seeking liquidity.